Stock Market: Artificial Intelligence Propels Global Markets to New Heights

Driven by the euphoria surrounding AI and colossal investments from tech giants, the MSCI World index continues its upward march. Despite a global economic slowdown and persistent inflation, the ultra-solid fundamentals of tech stocks—particularly semiconductor manufacturers—are currently brushing aside fears of a bubble. Here is an analysis of a fundamental trend that is reshaping the investment landscape.

Driven by the euphoria surrounding AI and colossal investments from tech giants, the MSCI World index continues its upward march. Despite a global economic slowdown and persistent inflation, the ultra-solid fundamentals of tech stocks—particularly semiconductor manufacturers—are currently brushing aside fears of a bubble. Here is an analysis of a fundamental trend that is reshaping the investment landscape.

After a strong rebound in April, equity markets maintained their momentum in May: the MSCI World index gained over 5% during the month. Hopes placed in AI are doing much more than offsetting fears of an economic slowdown and rising interest rates triggered by the war in the Middle East and surging energy prices.

Moreover, this rally in equity markets is made possible by the sheer size of mega-cap tech companies, mainly in the semiconductor sector (Nvidia, Micron, TSMC, AMD, Samsung, etc.). Their massive market capitalizations grant them significant weight in major indices, allowing them to pull the latter upward. In this context, it is easy to understand why American and Asian equity indices are rising faster than European ones.

Semiconductors: Colossal Profits Keeping the Dot-Com Bubble Specter at Bay

It must be said that these companies are capitalizing on massive investments in data centers and AI: we are talking about over $700 billion in investments announced by the Big Tech giants (Gafam) for this year alone! As a result, they are currently generating colossal profits and equally impressive growth. It is worth noting that this situation is very different from that of 1999-2000, when the "dot-com bubble" propelled often-unprofitable companies to insane heights.

To better illustrate and understand the current context, here are two striking highlights:

-

In terms of profitability: Companies like Nvidia, TSMC, Micron, SK Hynix, or Samsung Electronics are currently achieving operating margins of over 50%! However, let us not forget that the semiconductor industry is cyclical by nature: it is therefore highly likely that margins will not remain at these levels.

-

In terms of stock performance: Since the beginning of the year, shares of AMD, Micron, Intel, and Samsung have gained between 140% and 260%!

And what about valuations? In this area, it is difficult to call it a bubble. Yes, some stocks appear expensive (for instance, AMD trades at 93x earnings and Broadcom at 49x), but others are much less so: 15x earnings for Micron, 7x for SK Hynix, and 23x for Nvidia.

Correction Risks and Macroeconomic Slowdown: Key Points to Watch

Where does the economy stand in all of this? Well, growth is slowing down, as expected, both in Europe and the United States (Q1 GDP growth was revised downward to 1.6%), under the impact of rising interest rates, which dampen investment, and consumer caution.

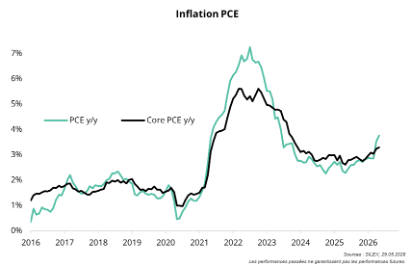

Meanwhile, inflation is ticking back up, to just over 3% in the United States, for example. Without reaching alarming levels, it still weighs heavily on purchasing power. Needless to say, markets would highly welcome the full reopening of the Strait of Hormuz.

Inflation Indices in the United States:

In Conclusion:

-

Risk factors are currently taking a backseat, as investors want to believe in the AI revolution and, above all, fear missing the boat (FOMO)!

-

Recent gains seem very/too rapid and increase the risk of a correction, or at the very least, heightened volatility in the coming months.

-

The situation is, however, very different from 1999-2000: the fundamentals of tech companies are far more robust today.

-

What is happening today (as has been the case for many years) reminds us of an essential rule: adopt a global investment approach, rather than a purely European one.